November 2024 ....The outlook for the sales market in 2025

The housing market has returned to growth in 2024, with more sales and higher house prices compared to 2023. The sales market has performed better than we expected a year ago, thanks to faster growth in household incomes and lower mortgage rates.

This report focuses on the prospects for the sales market over 2025 and the factors shaping the outlook. We expect house prices and sales volumes to edge higher over 2025 despite uncertainty of the impact of the Budget and whether mortgage rates will fall in 2025.

Lower mortgage rates support a return to price growth

Sellers (and buyers) returned to the market over 2024, building a healthy stock of homes for sale, which has supported sales volumes. The number of new sales being agreed is ending the year strongly, as serious buyers look to lock in sales in order to beat the return of higher stamp duty rates from April 2025. Sales agreed are 19% higher than this time last year, with buyer demand 25% higher.

More sales and greater buyer confidence have fed into higher house price inflation which stands at 1.5% in the year to October 2024, compared to prices falling by 1.2% a year ago.

House price inflation has now turned positive across all regions and countries of the UK, with the fastest price gains registered in Northern Ireland (6.3%) and the North West region (2.9%). Price inflation remains below 1% across southern England, where affordability pressures remain a drag on house price growth.

This north-south divide is evident at a local level, with the fastest price rises registered in the Oldham (OL, 3.7%), Wigan (WN, 3.9%), and Belfast (BT, 6.5%) postal areas. In contrast, modest price falls are still being recorded in pockets of southern England led by Ipswich (IP, -1.1%), Truro (TR, -1.2%) and Dartford (DT, -1.2%).

background image

+15%Growth in household incomes over last 2 years (nominal terms)

Stronger income growth repairs housing affordability

Last year we stated rising incomes would need to do the hard work resetting housing affordability in the face of higher borrowing costs. However, in 2024, income growth has been stronger than expected. The latest Office for Budget Responsibility (OBR) data shows household disposable incomes increasing by 15% between 2022 Q2 and 2024 Q22. House prices grew by just 1.5% over the same period, a trend that has helped to repair housing affordability without the need for additional house price falls. Incomes are forecasted to grow more modestly after 2025, according to the OBR forecasts.

background image

Data on home buyers using a mortgage shows the average household income of first-time buyers and existing owners has risen by between 9% and 12% over the last 2 years. In contrast, the purchase price and size of the mortgage have declined over the same period for existing owners as they adjust to higher borrowing costs. This trend is most notable in southern England, where higher mortgage rates have hit demand the hardest. In contrast, first-time buyers have made fewer compromises on the price of property they are seeking to buy while taking slightly larger loans.

16%Over-valuation of UK house prices in 2023

Mortgage rates to hold steady at current levels

Mortgage rates for home buyers have fallen by 1% in the last year to a current average of 4.1%. While mortgage rates have drifted higher in the wake of the Autumn Budget, we expect borrowing costs to remain at around 4.25% for a 75% loan-to-value 5-year fixed-rate loan.

In addition to the mortgage rate paid by a home buyer, lenders will also test new borrowers to see if they can afford a ‘stressed’ rate, which is currently closer to an average of c.8%. This has been a major affordability hurdle for home buyers as borrowing costs have risen.

We expect lenders to innovate around how they assess affordability for those taking fixed-rate mortgages of 5+ years, which will support buying power and levels of market activity over 2025 and into 2026 without any further reduction in headline borrowing costs.

Housing affordability improves over 2024

In addition to the economic outlook for jobs, incomes and borrowing costs, another key factor influencing the outlook for the sales market is whether current house prices appear cheap or expensive. The cheaper prices appear, the more likely they are to rise. Conversely, if homes appear too expensive, house prices are less likely to rise.

Zoopla has a model that tracks whether homes are under or over-valued. In 2007, at the time of the global financial crisis, house prices were over 40% over-valued and house prices fell sharply over 2008/9.

The jump in mortgage rates over 2022/23 led to UK homes being 16% ‘over-valued’ on the same measure. Strong income growth and lower mortgage rates have repaired this over-valuation over 2024 without the need for prices to fall (last year we expected a 2% fall over 2024).

Looking forward, we expect UK house prices to remain undervalued over 2025. This assumes an average mortgage rate of 4.25%, house prices rising by 2.5% and income growth of 4.6%. In the 3 years to the end of 2027, we expect house prices to grow by 7.5% in total.

83%Proportion of sales that will pay stamp duty in England and N Ireland from April 2025

Affordability a drag on price growth in southern England

Running the affordability model at a region and country level shows house prices are currently fairly valued in the Midlands, Northern England, Scotland and Wales. This explains why price gains are currently running at an above-average rate in these areas.

In contrast, house prices in southern regions appear over-valued by 30% or more, based on the average income for all household types. In reality, the incomes of mortgaged home buyers in the South are c.50% higher than average UK incomes. Running the analysis with the higher incomes of home buyers reveals a more modest over-valuation.

The challenge here is that the higher the income that is required to buy, the more households are priced out of the market. This limits the pool of demand for homes, and explains why house price inflation has experienced a slower recovery in southern England over the last year.

We expect house price growth in southern England to under-perform the UK average over 2025 and into 2026. Incomes need to grow faster than prices to improve affordability further in southern regions.

Stamp duty - an extra drag on house price inflation

Stamp duty is another factor likely to impact price growth over 2025. Many home buyers will pay higher stamp duty land tax (SDLT) from April 2025 in England and Northern Ireland, as the 2% band for owner movers returns and relief for first-time buyers (FTB) is scaled back.

Using buyer demand data, we estimate that half of existing owner movers pay SDLT today. It’s due to rise to over four-fifths (83%) from next April – with nearly all movers paying £2,500 more. The proportion of FTBs having to pay stamp duty from next April will double to 40%.

Buyers faced with higher purchase costs will want this reflected in the purchase price. This will act as a drag on house price growth over 2025, especially in the lower to mid-market price range (£125,000 to £250,000), where SDLT will represent 1% of the purchase price.

+5%Growth in housing sales over 2025

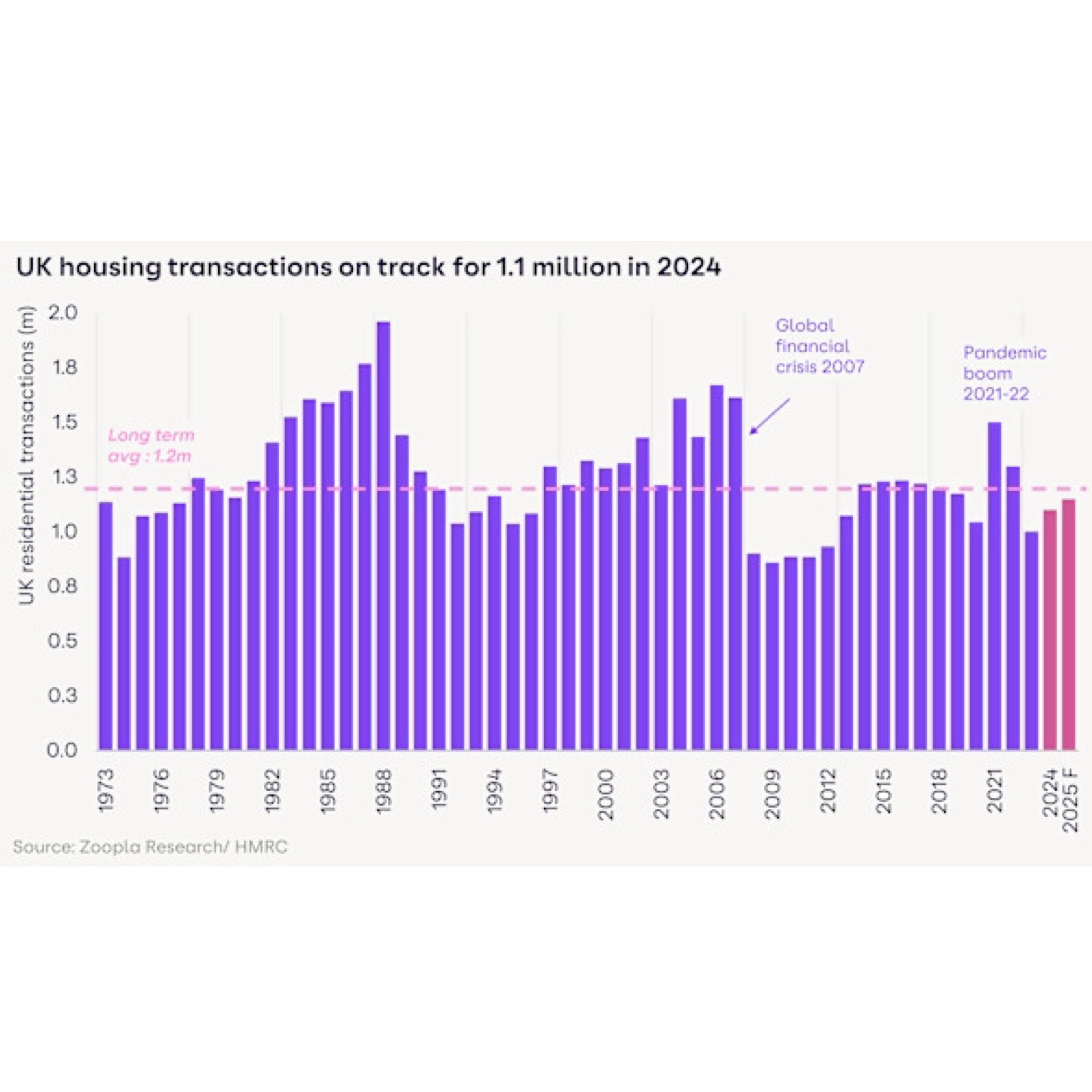

1.15m housing sales in 2025

The sales market is on track for 1.1m sales completions over 2024 – 10% higher than 2023. The pipeline of sales is also 30% larger than this time last year. This pipeline will support sales completions and deliver a boost in H1 2025. The key question is whether the current momentum in sales will continue over 2025. We believe it will, supported by rising incomes and changes in the way lenders assess affordability.

We expect further growth in sales over 2025 to 1.15 million, 5% higher than in 2024. First-time buyers will remain the largest buyer group, supporting housing chains and the ability of existing owners to move.

There is a wide range of motivations for people to sell and move home, which have become more rooted in needs-driven motives than aspirations. An ageing population, rising running costs and changing working patterns will continue to impact moving decisions, in addition to the desire to seek a better home or location.

Summary

The housing market has been very resilient in the face of higher borrowing costs over the last 2 years. Higher income growth and 4% mortgage rates have done much to repair headline affordability.

We expect house prices to rise by 2.5% over 2025, with sales agreed ending 5% higher at 1.15m sales. House price inflation in southern England will continue to lag behind the UK average. Incomes need to continue to rise faster than prices to help reset affordability and price more households into the market.

First-time buyers will remain an important buyer group, but existing homeowners looking to move need more support to help them realise their ambitions, with more and more having to look further afield to find better value for money.

Zoopla House Price Index, city summary, November 2024

Source: Zoopla House Price Index. Sparklines show last 12 months trend in annual and monthly growth rates – red bars are a negative value – each series has its own axis settings providing a more granular view on price development.

BU Homes are the leading, independent Solihull Estate Agent. We are a friendly, passionate team of local Solihull and South Birmingham property experts, based in Kineton Green Road in Olton, Solihull. Selling your home? Contact us for a free valuation today.